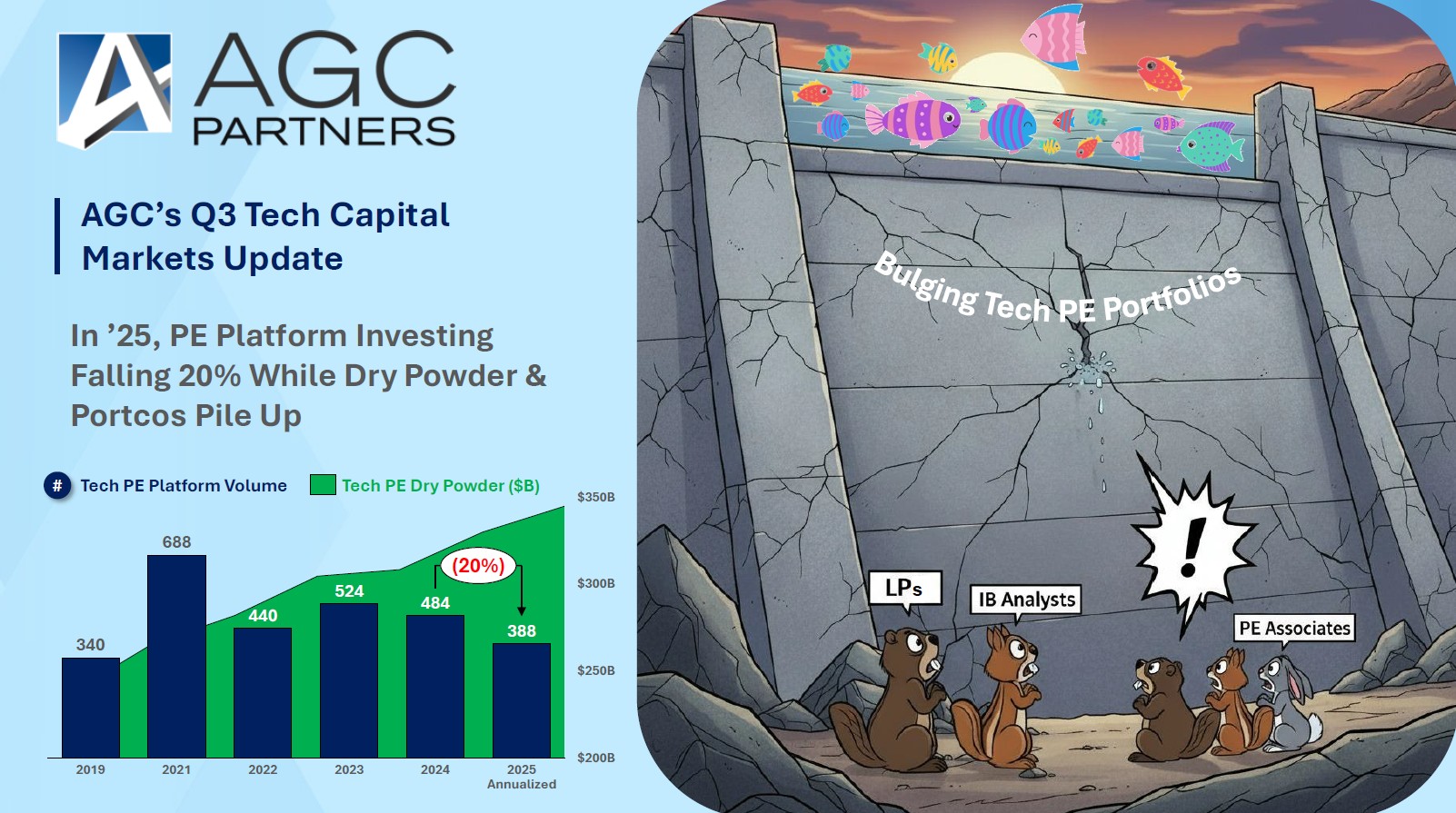

As software and global GDP growth continue to slow, the tech PE world in 2025 is struggling to both find new platforms and to exit current assets. New platform investments by the top 200 PE firms dropped 20% from 484 in 2024 to 388 in 2025. Exits remain depressed at 212 compared to 217 in 2024. These 200 PE firms represent 98% of the total tech AUM. New investments are running 2:1 over exits, which has helped drive portfolio holdings from 3,300 to 5,700, or up 74% since 2019. Simultaneously, PE GP fundraising has powered on at an unabated pace, up 46% since 2019, with tech PE dry powder growing from $237B to $345B today. Across the globe, there are just too many software companies that are chasing the same customers / TAM with similar products, and the market now requires consolidation, merging the underperformers and smaller players into the top performers and creating a healthier ecosystem with fewer companies and higher profits, albeit slower revenue growth. The obvious questions are: (i) when will these GPs start selling their assets at scale; (ii) what will be the pricing; and, (iii) who will be the buyers?

With tech PE portfolios ballooning to more than 5,700 companies and exits (including IPOs) tracking to roughly only 212 companies this year, our industry has a growing liquidity problem. PEs are hanging on to their portcos longer, in part to get back to their valuation marks, which may take until 2027 or possibly never. PE portcos have been very active, projected to close 1,100+ add-on acquisitions this year, but virtually all of these targets are founder- or VC-owned, not PE-owned. The PEs are the most likely and well positioned buyers for this mass of companies sitting around in plain sight. That said, the PEs are looking at their existing portfolio problem children and do not want to repeat the same mistakes – making them more reluctant buyers. The 169 public software strategics including Roper & Constellation will be in the buyer mix but they are on track to only buy 220 companies this year compared to the projected 1,500 total PE acquisitions. Tech PEs and their portcos are outbuying the public strategics 7:1. GPs are not confident that they will get their desired price and are holding back for now. Among the 5,700 portcos, there are many that are healthy – Ro30 or better companies, but the bid-ask spread is just too big, keeping these companies off the market for now. Rumor has it that Yale, which started investing in private equity in 1985 and which had never sold a position on the secondary market, sold $2.5B of its $10B in private equity in the secondary market at a more than 10% discount in June. If the PEs were willing to move off from their current valuation markers, the M&A market would open up. It may just take more time, more aggressive pressure from the LPs, or a recession that gives everybody a bit of a free pass to take lower returns.

With the stock market at record highs, valuations for public small cap similar companies that are 31 on the Ro40, trade at 3.4x revenue, and 16x EBITDA. Even the great companies that IPO, and came out hot, like OneStream at 10x, eventually drop back down to earth, currently at 5.5x. The roughly 100 small cap software companies trade at a 50% discount to the 70 large cap companies. Public institutional investors tend to steer clear of the sub $10B market capitalization tech companies because: (i) the companies underperform the larger peers over time; (ii) there is not enough liquidity in the stocks, so large block transactions are difficult to buy or sell without major price movement; (iii) it is difficult to get a meaningful enough position to make it worthy of the institutional investor's time; and, (iv) large institutions tend not to have the internal manpower to follow smaller stocks.

With PEs pushing off sale processes over the last three years, PE portcos have swelled to more than 5,700 – Battery, General Atlantic, PSG, and TA take the top spots with more than 100 active majority owned tech portcos each. PE portfolios really began to swell in '22 when SaaS market revenue growth collapsed. Since then, it has been difficult to impossible to sell middling to underperforming portcos. Not to mention the VCs who have tens of thousands of companies in their portfolios which are experiencing all the same challenges as the PEs. If PEs are hanging on to their best performers, then what companies will be performing well enough to bring to market in '26? The tech and PE industries are big enough for portfolios to keep growing, but we definitely need a lot more exits than we had over the last three years for the ecosystem to be healthy. There are whispers that Goldman is raising $1B in debt for Vista against Vista's flagship equity fund. The move is driven by two key objectives: (i) to provide meaningful DPI for LPs; and, (ii) to avoid selling underlying assets in an unfavorable market. This approach reinforces broader concerns that private equity firms are deferring exits without establishing third-party valuations, while simultaneously adding more off-balance-sheet debt to already leveraged portfolio companies.

While our software ecosystem adjusts and responds to the challenges of slower growth and constrained liquidity, the global opportunity for AI-enhanced software is larger than ever. The entrepreneurs, PEs, and bankers need to be willing to change their approach and rewrite their handbooks for a whole new set of circumstances and challenges. Kicking the can down the road with extended funds, CVs, off balance sheet debt, and other extension gimmicks does not address the underlying problems that require changes in the actual assets whether it is senior personnel, strategy, or sale of the business to name a few. If the leaders in our community can make those tough decisions sooner rather than later, then the sooner we can be unencumbered by the dead wood of the past to embrace and capitalize on the opportunities here today and tomorrow.

AGC is betting big on this global AI and software opportunity, with 24 new hires in 2025, and that is inclusive of leveraging AI into every nook and cranny of our business that we can ☺. As you see on the cover page of this report, we are already seeing cracks in the dam and a surge in activity, with an expected 25 deals closed this year, 33 new engagement wins, and 40% bump in revenues. With the increase in volume, deal selection is difficult, but we have been able to achieve a 9x median revenue multiple on our closed deals. After what we have seen since March of 2020, who knows what is next, but for now, we have the pedal to the metal. We hope you have enjoyed the read!

© In the U.S., America’s Growth Capital, LLC dba AGC Partners, member FINRA/SIPC. In Europe, America’s Growth Capital Europe, LLP (Appointed Representative Alternatives St. James, LLP which is authorized and regulated by the Financial Conduct Authority). America’s Growth Capital Europe, LLP is a Limited Liability Partnership incorporated in England and Wales (OC368580). Its registered address is 6th Floor, 9 Appold Street, London EC2A 2AP. The testimonials contained herein may not be representative of the experience of other customers or clients. Testimonials are no guarantee of future performance or success. Deals marked with an “*” are non-AGC deals.